MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

*I am bumping this up to the top of the blog roll as I added a section towards the bottom of this post regarding a new benefit coming August 1 that could be a largely influential factor in whether or not you keep your SPG Amex Card open. Thanks to Reader Jon for reminding me.*

I hold both the Starwood Preferred Guest Credit Card from American Express and the Starwood Preferred Guest Business Credit Card from American Express. I opened the consumer card a little more than a year ago, so the second annual fee was just charged (the first year’s annual fee was waived as part of sign-up package). That meant it was time for a cost/benefit analysis. I imagine many of you are at the same crossroads, as the elevated 35k bonus offer for the SPG card ended April 5, 2017.

If you’re not already, get yourself in the habit of performing cost/benefit analyses when annual fees come up for your cards. Mindlessly paying annual fees without considering the return from the rewards you’re earning as well as the value of benefits will slowly chip away at the value of your rewards over time.

No Matter What Your Situation, Perform a Cost/Benefit Analysis

A cost/benefit analysis will help answer the question of whether or not you’re getting enough value from the card to continue holding it. Assuming you don’t need to close the card for the purpose of opening another, here are the first two steps.

- Are you getting a retention bonus for keeping the card that is worth more than the annual fee? If so, keep the card. If not, I go to step 2.

- Are the marginal benefits of holding the card larger than the annual fee. If so, I keep it. If not, I cancel it.

Both steps come down to future-looking value. The annual fee is a cost, and I need to get a benefit at least as big as that cost ($95) by keeping the card.

What I Already Knew Considering Upcoming Changes August 1

I already knew that if I didn’t manage to pull a retention bonus from Amex that at least outweighed the $95 annual fee, without any no-annual fee card options to downgrade to, then I would cancel. Why? Because the reward earning structure on the SPG Amex cards is devaluing come August 1 when Marriott and SPG merge their loyalty programs. Instead of earning the equivalent of 1 SPG point per dollar spent on non-bonused purchases, that will change to the equivalent of .66 SPG points per dollar spent on non-bonused purchases. 1 SPG point = 3 Marriott points, and all existing SPG points will be converted to Marriott points at that rate on August 1.

You will earn 2 Marriott points per dollar spent on everyday spend, but the conversion rate of Marriott points to most airline partners will be 3:1. So while you may have your choice of TONS of airlines transfer partners come August 1–even more options than you have with SPG now–not even earning 1 mile per dollar is just not good enough. And transferring SPG/Marriott points to airline partners is the sole reason I collect SPG/Marriott points.

If the earning rate had effectively remained the same, 3 Marriott points per dollar on everyday spend, then I would have without a doubt kept the card open for all my non-bonused spending. Sadly that is not the case.

But it’s not August 1 yet, so there is still time to earn 1 SPG point per dollar (a point I highly value at 2.5 cents each due to the myriad of airline transfer partners), and I’d unsurprisingly seen reports of lucrative retention offers for the personal SPG Amex Card.

While Amex will acquire new customers with its premium ($450/year) SPG card due out in August, that’s a different subset of customers than those spending on their $95/year SPG Amex cards. Amex is at risk of losing those customers to Chase, who have just recently introduced a new consumer Marriott credit card at the $95 annual fee level with a 100,000 point Marriott bonus. Hence the higher probability of valuable retention offers for the personal SPG Amex.

Circling back to what I stated above, as long as you don’t need to close the card for the purpose of opening another, no matter what you have decided regarding a credit card that’s in question you should always call for a retention bonus to see what you’re offered. Here’s what happened when I called Amex.

Calling in for the Bonus

There are two more steps I recommend taking before calling in.

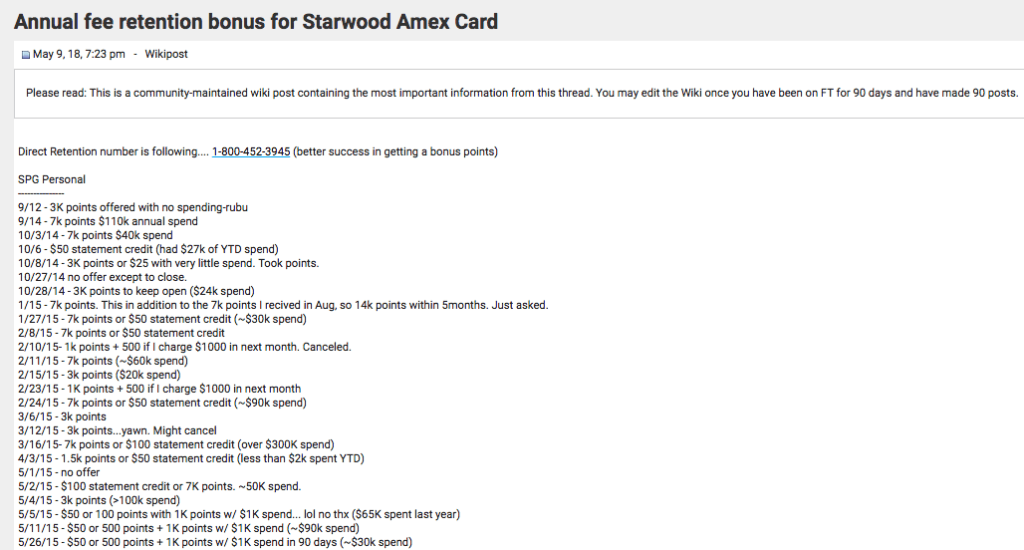

- Do a little research first to see what others in your shoes are being offered. I recommend googling “flyertalk retention offers [insert your card here]”. This should turn up a link to a Flyertalk Forum where others list what retention offers they’ve received for your same card, listed by date. For example, here is the wiki for the SPG Amex Retention Bonus forum…

If you can get an idea of the best most recent offer on the table, then you’ll know to keep asking for more offers if you get a lesser one first. Scroll down to the bottom of the wiki and you’ll see almost all data points report an offer for 7,000 SPG points for spending $500 to $1,500 within a month to three months of accepting the offer.

- 1/17/18: Personal Card. Offered 7000 SPG points for $1,500 spend in 3 months. Took offer.

- 2/23/2018: 7k points for 1k spend in 90 days. 7.5k annual spend

- 3/27/2018: 7k points for 1k spend in 90 days. Took offer.

- 3/30/2018: no retention offer. Got 10k last year, minimal spend since then. Would not allow product change.

- 4/13/2018: 7k points for $1.5k spend in 3 months

- 4/20/2018: 7k points for $1k Spend in 1 month. Accepted.

- 4/26/2018: 7k points for $500 spend in 1 month. Accepted.

- 4/28/2018: 10k points for $1k spend in 1 month. Accepted.

- 5/1/2018: 40$ to offset annual fee. Accepted

- 5/6/2018: 7k points for $500 spend in 1 month. Rejected.

- 5/9/2018: 7K points for $500 spend in 1 month. Accepted. ($15K spend in 2017)

2. Know how much you value the point your card earns. Read How Much Are Frequent Flier Miles Worth? Calculating your Own Valuations to learn how to do it yourself, or if you’re feeling lazy use mine.

Armed with all of the above knowledge, ready to keep pushing until I got the 7k points for $500 spend, I called the number on the back of my card. According to the wiki on the Flyertalk thread it’s even easier to get bonus offers by calling 1-800-452-3945 instead, but I missed that on first glance.

What I Was Offered

Right out of the gate, I was offered 7,000 SPG points for spending $500 within a month. Out of curiosity I asked if there were any other offers, and was also given the option of a $75 statement credit for spending $2,000 within two months of accepting the offer. For reference, I’ve put $12,800 in spend on the card since I opened it a year ago.

Some quick math told me:

- 7,500 SPG points (how many I’d earn for the $500 spend + the bonus points) is worth about $187.50 to me…

7,500 x .025 = $187.50

That would leave me $92.50 ahead after taking out the cost of the $95 annual fee.

- a $75 statement credit would leave me $20 in the hole after the $95 annual fee.

Pro tip: If you ever get a rep who doesn’t offer you anything, ask to speak with a specialist that can give you more options. That question will, nine times out of ten, get you on the line with the retention specialist who’s job it is to keep you a customer.

My Decision

I already have a nice sum of SPG points, so an additional 7.5k would be very welcome. I can easily find a high value use for them. Not to mention the additional value of keeping the account open for the sake of my credit score. Keeping my SPG Amex open another year will increase the average age of my accounts and help keep my *credit utilization ratio low.

I took the 7k bonus points for $500 spend offer.

*How much you owe compared to how much credit you have available total.

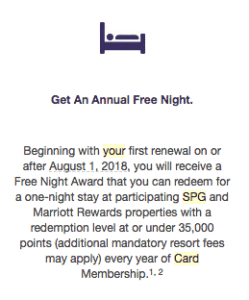

The New Benefit as of August 1 That Might Make it Worth Keeping Card Open

If you have an SPG card, you should have gotten an email mid-April outlining the changes coming to your card as of August 1. The most interesting one that might convince you to pay that annual fee another year is an Annual Free Night.

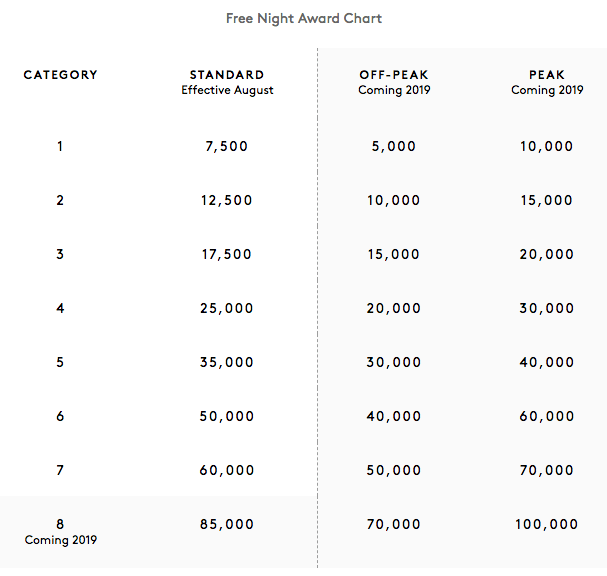

You can stay at any Marriott / SPG property once a year for 0 points, as long as it doesn’t cost more than 35,000 points per night. That’s a category 5 hotel or lower, as long it’s not during Peak travel season.

Personally, this benefit isn’t worth anything to me because I’m not a Marriott / SPG hotel patron, nor really a hotel patron in general. I collect Marriott / SPG points specifically for transferring to airline loyalty partner programs. I prefer Airbnb for travel accommodation, and if I ever do stay in a hotel it’s not a chain…simply due to the fact that if the area is remote enough not to have good Airbnb options, then it doesn’t have chain hotel options either. Therefore I’d likely have to spend money to be making use of this benefit, as I can’t think of many circumstances in which I’d want to stay in a hotel for just one night.

That being said, if you do patron Marriott and SPG hotels properties and use points for hotel stays, then this benefit will likely do exactly what it’s meant to do: entice customers like you to keep the card open. You’re the loyalty member they want, not me. Makes sense.

So when you’re doing that cost/benefit analysis, remember to factor this new Annual Free Night benefit into the equation.

Bottom Line

I am going to spend $500 on my Starwood Preferred Guest Credit Card in the next month, leave it in my wallet for non-bonused spend through the end of July, and then I’ll take it out of my wallet and let it sit in my closet until April of 2019. I have no incentive to spend on it past July when the earning rate will fall to only 2 Marriott points per dollar spent on everyday purchases. It takes 3 Marriott points to transfer to 1 airline mile, so…no thanks.

I’ve set a Google Calendar alert to send me an email in early April of 2019, when the next annual fee will be charged, with a reminder to take another look at whether or not the card is worth keeping open another year and to call Amex for another retention bonus either way.

If you find yourself in the same boat, I recommend calling Amex to see if you can get the same 7k bonus for $500 spend. It seems to be the offer du jour. Share any offers you receive in the comments!

I had the Biz card AF due last week and been calling few times for retention but no dice……So I will cancel the card this weekend.

Yea, unfortunately haven’t seen many recent retention offers for the biz version 🙁

This article save me big time! No retention offer on SPG biz, but saved me paying $95 AF for a loss of 2 major perks

Have you been putting $30k/year on your card? I wonder if that makes a difference.

Thanks for this vital column, Sarah…

Your thoughts triggered two questions.

1) With the pending devaluation of the SPG points, should one consider emptying one’s SPG account by transferring them to our most frequently used airlines, hotels, etc., before they lose value? And,

2) Which card(s), outside of Chase cards, offer the best transfers options? I have always used my SPG Amex as my main card due to its “transferability.”

Thanks and keep up the good work

You are welcome, Tomm!

1) SPG points are not devaluing. As of right now, 1 SPG point = 3 Marriott points. Come August 1, all your SPG points will be converted to Marriott points at that same 1:3 rate. The transfer rate between Marriott points and all those same airlines SPG points are able to transfer to now (plus even more) will be 3:1. So you don’t need to move your SPG points anywhere… you’ll still be able to transfer them at the same rate post August 1. The only exception is direct Marriott to United transfers (or buying United Marriott Travel Packages), which is devaluing. If you want to do that, complete the transfer before August 1.

What I referred to in this post as devaluing is the earning rate on your SPG cards (value of actual points remains more or less the same in terms of transferring to airline partners). Instead of earning the equivalent of 1 SPG point per dollar on everyday spending (3 Marriott points per dollar spent), you will earn 2 Marriott points per dollar spent. And that’s no bueno.

Still confused? Read What August 2018 Holds For Marriott/SPG: Part II

2. The answer to this question is not so straightforward and is going to depend on the consumer. I agree, before it was an easy answer. But not so much come August. Will be diving deeper into this at some point here on the blog, so keep an eye out.

That being said (re #2), if you are able to open business cards, there is an easy answer for all non-bonused spend…the Blue Business Plus Amex. But if you have a ton of non-bonused spend (upwards of $50k), then it gets more complicated because that’s the cap for the 2x bonus on all purchases with the Blue Business Plus. Like I said, more to come…

I got a 10k for $500 spend offer, or the $75 for $2000 spend.. so, yeah, I didn’t take the $75 one.

Apologies if I’m completely confused, but aren’t they adding a free night’s stay each year? Unless I’m mistaken, that should make up more than the annual fee (WAY more, in some cases, as I thought I read that the free night could be used for rooms costing up to 30k spg points, which I have seen for $700-$800+ per night).

Am I missing something? I would think that would make keeping the card a no-brained.

You’re right Jon, and I should have mentioned that new benefit in this post. But no, that doesn’t make keeping the card a no-brainer for me. I pretty much always use Airbnb when traveling, and if I do stay in a hotel it’s because the area is remote enough that Airbnb hasn’t really hit there yet and the only options are tiny mom and pop type bnbs or boutique hotels. I wouldn’t ever use this benefit, because chances are I’d want to stay in said hotel for more than one night..so I’d end up spending money to “save” it. All that being said, for those that do patron Marriott/SPG properties, this benefit could very well make it worth keeping open. Will update post to mention it, thanks for pointing that out. And you actually can stay one night in properties that cost up to 35,000 points.

Also, depending on the timing of your fee (like, if it’s this month), you’re paying the fee for no benefit, because the free* nights don’t start until August.

* $95. Not actually free.

My anniversary is in August. If I keep it I’m basically paying $95 to stay in an average hotel room.

Right now my thought is to cancel.

I know what you mean about using Airbnb instead, but I find these free night stays perfect for when I am arriving or leaving and need to spend a night near the airport when it’s less practical to use Airbnb.

I had the Marriott free cert for a while and it wasn’t a high enough category certificate to even get me a room near an airport in a major city. Most airport hotels have a pretty high category, so you have to stay far from the airport.

Also I am irritated that people with renewals between now and August don’t get a certificate until they pay $95 2 more times.