MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

This week I helped my dad decide what to do with his Platinum Card® from American Express.

These are the questions I pose when looking at year two of a card with an annual fee.

Are you getting a retention bonus for keeping the card that is worth more than the annual fee?

The retention bonus he was offered was not worth more than $550 annual fee, as he did not put a significant amount of spending on it past meeting the minimum spending requirement. Moving on to question #2…

Are the marginal benefits of holding the card larger than the annual fee? If so, keep it.

He used the $200 incidental airline fee credits, bringing the effective annual fee down to $350. But he didn’t utilize all the Uber credits, already had Global Entry credited from the Sapphire Reserve (a card he doesn’t plan on canceling in the foreseeable future), and wasn’t traveling through airports often with Centurion lounges, which are the major benefit over the Priority Pass lounges you get access to with other premium cards. Nor does he buy tons of cash flights or hotels, so the 5x category bonus for travel booked through Amex’s portal isn’t particularly rewarding.

If the marginal benefits aren’t worth keeping it open, is it a card that earns rewards that will expire if you cancel it? Airline miles don’t expire if you cancel a card that earns them. But transferrable bank points (like Amex Membership Rewards, Chase Ultimate Rewards, and Citi ThankYou Points) will expire if you cancel the card that earns them.

The Platinum Card is one of those cards whose points–Membership Rewards–will expire if he cancels the card.

If canceling means losing points, than look at transferring them to a transfer partner you know you will you use, or another account within that bank’s loyalty program before you close the credit card.

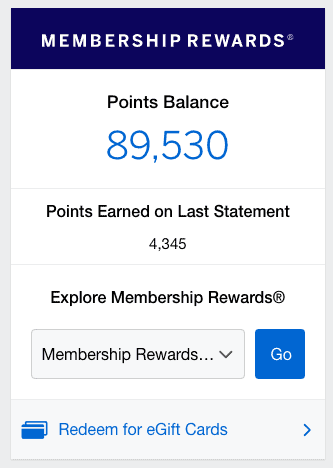

He’s got almost 90,000 Membership Rewards left in his Platinum Card® account. With no travel plans on the horizon at the moment, transferring them all to an airline partner feels like putting all his eggs in one basket. So we looked at other options to keep his points alive as is.

He doesn’t have another Membership Rewards-earning Amex card. The downgrade options (that must be charge cards as the Platinum is a charge card) –an Amex Green or Amex Gold Card–are not ideal. Downgrading to the Gold would still incur a $250 annual fee, and you miss the sign-up bonus by downgrading instead of applying outright. The Green Card is an ok option, but still has a $95 annual fee and crappy benefits (just 2x points on purchases booked through Amex’s travel portal).

So we looked at his options if he opened a new card.

The Decision

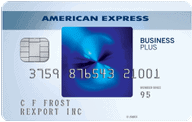

We landed on the Blue Business Plus Credit Card from American Express, which has no annual fee (big win) and earns 2x points on everyday business purchases (the first $50,000 spent per year). He runs his own consulting business so business cards are not foreign. And the points it earns are Membership Rewards, transferrable to all the Membership Reward airline transfer partners, so in that sense his existing points will not devalue.

And if you’re trying to fly under 5/24, business cards from Amex will not count in your Chase 5/24 total.

All Membership Rewards earned by a person are pooled in the same account automatically (within your Amex online account) as long as each card is linked to the same Amex account. Once my dad opens the Blue Business Plus, we will make sure his card is linked to his existing Amex account that his Platinum points are in, and then he’ll be set to cancel the Platinum. The annual fee was already charged on his Platinum, but you have a month after the closing date of the statement it was charged in to get a full refund if you decide to cancel.

Bottom Line

If you are eligible for business credit cards–which you may be and not even realize–and need a home for Membership Reward points that would otherwise evaporate thanks to account closure, I think the Blue Business Plus Card is the best option for preserving the life of your Amex Membership Rewards. You don’t have to pay anything for it as the card has no annual fee, and the ability to earn 2 Membership Rewards on all otherwise non-bonused spending is huge. It’s a card worth getting even if you don’t need a home for Membership Rewards.

Huge cost for a card after the first year hard to get Value . I have the same deal with my Thank You points . So United works for me so I will transfer all 76k points to Singapore Airlines . Then I will cancel the Premier card after 9 months but keep the Prestige card till 7/2020 . I’m afraid Citi will get ” Funny with the Money ” and take back points that are intermixed . Plus less cards I have I’m setting myself up for a high points offer when it happens .

CHEERs

“And if you’re trying to fly under 5/24, business cards from Amex (nor from most issuing banks except for Capital One) will count in your Chase 5/24 total.”

This seems to be worded wrong or very confusingly. Is it counted or not counted towards 5/24?

Thanks for pointing that out, left out “not” in that sentence. Edited for clarity: “And if you’re trying to fly under 5/24, business cards from Amex will not count in your Chase 5/24 total.”

At some rare times Amex Blue for Business Plus has offered 10000 MR points bonus. My wife and I both caught a very rare bonus offer for 20000 points bonus. I forget but I think 20k was targeted. Sometimes a referral bonus is also possible.

I agree with Larry – you can get 10,000 points as a signup bonus if someone refers you to the blue business plus. It’s still available, I can share a link if anyone wants an extra 10K!

Thanks Larry and TJ for pointing that out. I decided to delete my prior sentence about the Blue Business Plus not having a sign up bonus because it was misleading anyways… you can’t downgrade from a Platinum to a Blue Business Plus.

Amex Everday?

You can’t downgrade a Platinum to an Everyday card because the Platinum is a charge card and the Everyday is a credit card. He could’ve opened one outright, but I think the earning structure on the Blue Business Plus is more lucrative longterm than the Everyday. If you can’t open a business card, then the Everyday could be a good option to preserve your MRs.