MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

When you get deeper into the world of opening rewards cards to get free or luxury travel, there is an inevitable amount of bookkeeping that comes with managing your credit cards.

You have to track:

- when you opened each card

- when the annual fee is due on each card

- how much you’ve spent toward the minimum spending requirement associated with the sign up bonus

- when each statement closes

- when payments are due on each card

- category bonuses

While that looks like a lot to track, and may seem daunting, I estimate that I spend about 30 minutes per month on everything credit card related.

I think about a credit card’s life cycle as having four stages:

- Application

- Getting the bonus (minimum spending)

- Regular use (category bonuses)

- Renewal/Cancellation

Here’s what I do at each step to keep track of my cards and minimize my headaches.

What are the steps you need to take to put your credit card tracking on auto-pilot?

1. Application

I keep the time spent on applications as low as possible by applying for any cards I want on the same day (and making these days at least 91 days apart.)

Once I complete an application day, I note 91 days later on my phone’s calendar, so I know when I can apply for new cards.

I spend a lot of time every day thinking about the best credit cards for travel, so it doesn’t take me any extra time to pick out the cards I want. But for a regular person, planning which cards best suit their travel goals could take a lot of time because the Best Cards for Big Spenders differ from the Best Cards for Small Spenders, which differ from the Best Cards for Economy Travel.

How MileValue Can Help Save You Time Planning Your Application

I offer a Free Credit Card Consultation. Fill out the form with relevant details about your travel goals, spending patterns, and where you live, and I’ll tell you the best cards to meet your goals.

2. Getting the bonus

Once the cards come in the mail, it is time to set up your online banking to save time in two ways: by automating bills and by making spending easy to track.

Setting up online banking for the first time is easy on each bank’s website. Adding new cards to an existing online account can be automatic or a few clicks.

Adding New Cards to Existing Accounts

In the past year, I’ve gotten cards from six banks:

- Chase

- Barclaycard

- Bank of America

- US Bank

- Citi

- American Express

If you sign up for a new card with an existing online banking account, Chase, Barclaycard, and Bank of America will automatically add your new credit card to your existing online banking account.

Simply sign in and you’ll see the new card. Then set up a recurring monthly payment to pay your bill in full online from your bank account. They should also have your bank account info stored if you have automatic payments set up for another credit card.

Setting up auto-payments in full is a crucial time saving step. If you can’t do it because you’re not sure you can pay your credit cards in full each month, do not open any rewards cards. The interest on rewards cards will far exceed the value of the rewards.

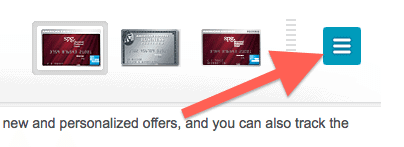

Annoyingly American Express and Citi do not automatically add new cards into your account. With American Express, it takes two clicks plus the card number to add a new card to an existing online account.

On the home screen of your account, click the teal box next to your existing cards.

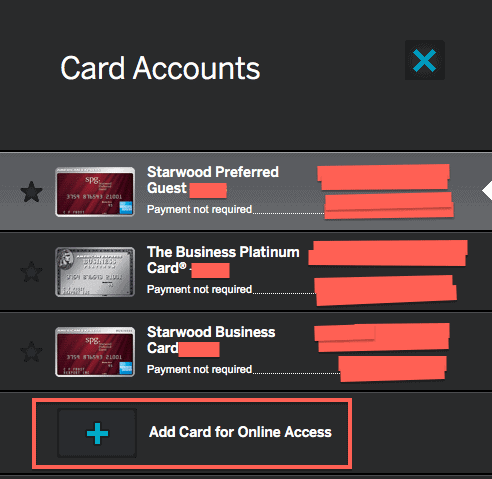

Then click Add Card for Online Access on the popout screen.

Then click Add Card for Online Access on the popout screen.

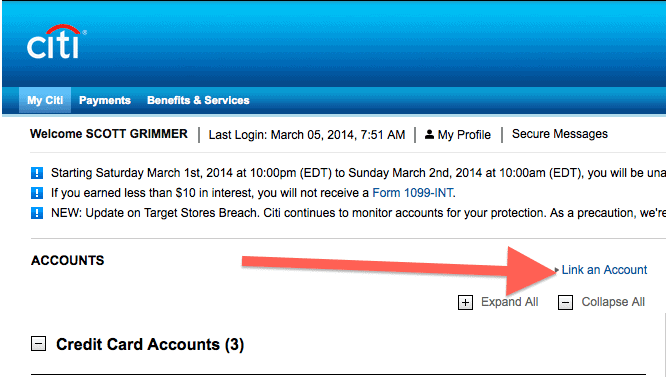

For Citi, click Link an Account on your account’s home screen.

Unfortunately I haven’t figured out how to add new cards to my existing US Bank online account. I better get on that. Any tips?

Once you have your cards in the account, set up a recurring payment. Citi and American Express make you re-type in your bank account info for each credit card.

Tracking Spending

Tracking whether you’ve met a card’s minimum spending requirement takes some effort. I’ve laid out my strategy on How to Meet Multiple Minimum Spending Requirements at Once before.

3. Regular Use (Category Bonuses)

Almost all the time in managing cards will come during applying and meeting their minimum spending requirements. Once we get past those stages, there is very little left to do.

Your monthly statements are all online. You can look at them however often you want to ensure no fraud is occurring. That should be very little time.

The time you’re spending on cards during this period is remembering when to use which card to maximize category bonuses. This should take no time at all.

Either memorize each card’s category bonuses or write them on the card. I bought some tiny circular stickers at the dollar store, wrote the card’s category bonuses, and affixed them to the front of my cards when I was just starting out with rewards cards.

4. Renewal or Cancellation

As soon as I apply for a card, I make a not on my phone’s calendar for 11 months later to decide whether to renew or cancel a card.

When my phone beeps to tell me to make the decision, I weigh: Should I Keep This Card? Whether to Hold or Cancel a Rewards Card When an Annual Fee is Due.

If I decide to cancel the card, I’ll call in. If I am offered a good enough retention bonus to change my calculation, I’ll keep the card.

If I still want to cancel the card after talking to an agent, then I will transfer out any points that would disappear when the card is cancelled before cancelling the card. (Note that hotel and airline points are safe. Only bank points are at risk during credit card cancellations.)

If I keep the card, I will make a note for one year later on my phone to make the decision again whether to keep or cancel my card.

Recap

I estimate that all of that–applying for cards, tracking bonuses, setting up online banking, and deciding whether to cancel cards–averages out to about 30 minutes per month.

And there are ways to reduce the time you spend thinking about cards, like by getting a Free Credit Card Consultation.

This doesn’t include keeping track of all my rewards, planning trips, award booking, or going on all my free vacations. That takes more time, but that’s all fun for me.

If the rewars-managing side isn’t fun for you, there are also ways to reduce this amount of time to basically zero–other than the free vacations–by using Award Wallet and my Award Booking Service.

Just tracking cards takes time, but not all that much time. How much time does tracking your cards take you? What are some time-saving tips?

I’ve had regular Chase cards and recently got an Ink business card. The Chase site won’t let me link my Ink card to my account, saying: “We are unable to process your request because the Account Number you entered cannot be linked to your profile.” (We can’t do it because we can’t do it!) So I’m “secure messaging” them to try to get it added. Do you think this is because it’s a business card?

Yes, Rachel is correct. I should have noted that Chase personal and business accounts are separate. VERY annoying.

@Scott – Not true. We called Chase for my wife’s accounts and they very easily combined her business (Ink) and personal (BA & Freedom) cards into one online profile/login. @Jill – It just errors out online, if secure message doesn’t work, give them a quick call. Took us less than 10 minutes to resolve.

Thank you! I appreciate everyone’s help.

Great tip!

@Jill,

Yes, you will need to have a separate business account with Chase.

You need to remove the word “To” in the title of this article. 🙂

Yes. I’ve had the same issue before. They cannot be combined.

With Chase after you open your online Business account you can then add your personal accounts to it.

Good tip! I’ll do that next.

I’ve been using Quicken since 1998 and it has been invaluable for this. I currently have 17 cards open and download transactions every day in one shot for all of them. This makes it easy to track fraudulent charges immediately if they show up. I also have made all the payment dates the same to simplify. I refuse to let any company come in and deduct money from my accounts to pay bills, whether credit card or other (especially since I pay bills often with Bluebird). Using the Quicken online bill pay via Bank of America I can pay all my bills when I get them but have them dated to the due date.

Another annoying Citi policy: You can’t link a personal HHonors Reserve card to the same account as other personal cards (such as AA). You need to create a separate online account for it.

for those of us that aren’t accountants do you have a spread sheet to share?

Scott, I usually put the the 11 month deadline on my phone so I can call but I forgot to with my Sapphire Preferred as I planned to keep it. Any experience calling for a retention bonus post getting hit with the fee? Worth the effort?

This has been great info. Could you write something about how long you can keep your bonus miles after you cancel a card and how long after you cancel it can you re-apply for the same card and get the bonus miles. I am running out of cards to apply for and want to try this with Aadvantage Visa, United Airlines Mileage Plus, Chase Sapphire, US Airways Barclays, Delta Blue [changed from AMEX because didn’t want to pay annual fee] and British Airways Chase.

@Sara, I almost always wait until I see the fee on my statement, then call. They have always removed or reimbursed the annual fee if I end up canceling the card. I can’t say whether or not there would be a different retention bonus, but often there is one, and the offer to downgrade to a no-fee card is pretty common too. I suppose the 11-month idea would be better; I guess I’m just not quite as organized as some.