MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Update: Chase is now responding to people complaining on Twitter that IHG credit card accounts opened from January 1, 2018 through April 5, 2018 (that’s tomorrow) will be able to use their Free Night Certificate once with the old terms (meaning at ANY IHG property, not capped at a 40k point property). Apply now if you want that Free Night Certificate! Hat tip to Mommy Points.

One of the most valuable perks of the IHG Rewards Club Select Card that made the card worth keeping year after year is the annual Free Night certificate (based on cardmember year) that was redeemable at ANY IHG property. Getting outsized value from this certificate made it more than worth it to pay the $49 annual fee.

IHG has not only changed how the Free Night certificate can be redeemed for new card applicants, but also–much to their chagrin, especially those who applied just before the change expecting to get grandfathered in to the old terms–for existing cardholders.

As of May 1, 2018, any Annual Free Night certificate issued will only be redeemable at properties that cost 40,000 points or less per night. You can see the list of excluded properties here, which oddly includes various 40,000 point/night or less properties.

If you are an existing cardholder, hopefully your Free Night Certificate was already issued this year or will be issued before May 1, 2018. Then you can at least, once more, use it any IHG property. After that you’re out of luck and may want to reconsider keeping the card open longterm. When your Free Night Certificates are issued depends on when you signed up for the card as they are an anniversary bonus.

Thoughts on the Devaluation

I tend to agree with Rapid Travel Chai here. I doubt most people put much/any spending on this card–they pay the annual fee each year, stick it in the back of their sock drawer, and forget about it. So the devaluation of the Free Night Certificate benefit should not come as a shock. I’d assume IHG was losing big money with the ability to redeem the certificate on properties like the InterContinental Bora Bora Resort Thalasso Spa, pictured above.

Of course it’s unfair to loyal IHG customers/those putting significant spend on the card, but I’d bet that doesn’t apply to most. So yea, any devaluation sucks, and this one hurts because it was an especially sweet perk for a card that costs a mere $49. But I’m not surprised the benefit was capped.

What I do find to be dishonest on IHG’s part is the fact that various properties that actually cost 40,000 IHG points or less are on the list as excluded. Yet in their marketing they claim the certificates can be redeemed at properties that cost 40,000 points or less.

And the letter sent out to existing cardholders states, “Going forward, Anniversary Free Nights issued after May 1, 2018 will be redeemable at eligible IHG properties with a redemption value up to and including 40,000 points.”

Still Worth Getting?

Now that the most valuable benefit of the IHG Rewards Club Select Card is gone, is this card still worth getting?

Maybe, primarily for the bonus which you can use at PointBreaks hotels. PointsBreaks hotels–their rooms they put on sale for only 5,000 points a nigh– are perhaps the best use of IHG points. IHG Rewards Club normally charges 10,000 to 70,000 points for a free night depending on the property. But every few months, IHG Rewards Club releases a list of a select few hotels where you can stay for 5,000 points per night. That’s a 90%+ discount on some hotels.

The current list of PointBreaks hotels is good for stays through April 30, 2018, and a new list should be coming out in the next few weeks.

On PointBreaks, I can get over one cent of value per point, but those have such limited capacity, that I will conservatively value IHG Points at 0.6 cents each. That makes 60,000 points bonus worth $360. That’s an ok bonus, but not great.

If the PointBreaks list has hotels located in destinations you are interested in traveling to, and the hotels happen to be expensive on the dates you want to travel, then the IHG card is still a no-brainer. You can use the 60k bonus for 12 free nights at 5k/night PointBreaks hotels. If the rooms you want on the days you want them are cheap, then it’s probably not worth it.

While the infamous Chase 5/24 rule is known not to apply for this card, keep in mind that opening it will count towards your 5/24 total as it is a personal credit card.

Quick Facts on the IHG Rewards Club Select Card

- Sign Up Bonus: 60,000 IHG points after spending $1,000 in the first three months

- Category Bonuses: 5 points per dollar spent at IHG properties; 2 points per dollar spent on purchases at gas stations, grocery stores, and restaurants

- Cardmember Anniversary Bonus: Free night at eligible IHG properties

- Elite Status: IHG Platinum status

- 10% rebate on IHG points you redeem each year

- No foreign transaction fees

- Annual fee: $49, waived the first year

- Eligibility: Not subject to Chase 5/24 rule

Bottom Line

The most valuable benefit of the IHG Rewards Club Select Card, a Free Night Certificate after cardmember anniversary each year at ANY IHG property worldwide, has been capped. Any certificates issued after May 1, 2018 will only be valid at properties that cost 40k points or less (and cannot be redeemed at these properties, some of which cost 40k points, which I find to be non-transparent and annoying).

Whether or not this card is worth getting anymore depends on if you have a high value use for IHG points, as the bonus is now the main selling point. Typically the best use of IHG points are PointBreaks Hotels, which are priced as low as 5k points/night.

What do you make of this change? Are you going to keep your IHG Rewards Club Select Card open another year?

Thanks for the heads up on this change from reader Buzz W.

where are you getting the information that Holiday Inn Phuket Mai Khao Beach Resort rooms go for 15k / night? They show 25k.

Uhm, your link shows excluded hotels that cost more than 40k.

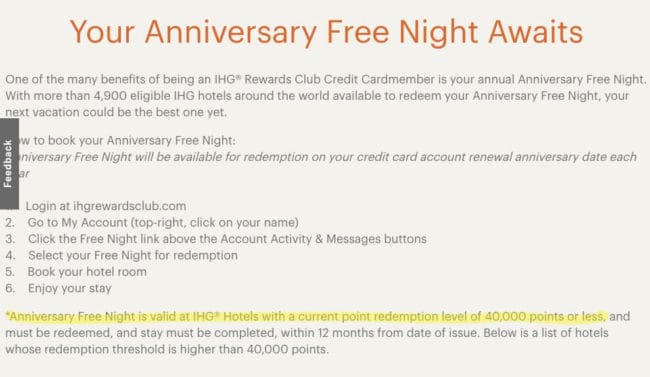

*Anniversary Free Night is valid at IHG® Hotels with a current point redemption level of 40,000 points or less, and must be redeemed, and stay must be completed, within 12 months from date of issue. Below is a list of hotels whose redemption threshold is higher than 40,000 points.

Well that is what it says, but it’s not the reality. There are properties listed there that cost 40k or less. Examples: Intercontinental Prague, and Holiday Inn Washington-Central/White House.

i dont see any hotels listed there r under 40k …even if so maybe be ihg mistake on their end since term clearly stated cert only valid on 40k or less..

Chase’s response is confusing. I got my card in July 2017 so I don’t get the unlimited free night on my anniversary but someone who applies now does?

If that’s the case I’ll take my cheapo free night and burn the rest of my points and cancel the card.

That is what seems to be the case, and yes it is confusing. I would try directly tweeting at Chase with a complaint to get the Free Night cert anywhere once more.

To be ethical, they need to give the free night on the old terms to EVERYONE based on the terms in effect when they last paid the annual fee. To make a change going forward – effective with the next renewal – would be disappointing, but acceptable. I wonder, though, if it’s even legal, much less ethical, for a bank to change the terms of a credit card offer after accepting a fee for one.

We all knew this day was coming.

$49.00 to stay at the Sydney Intercontinental has been a great deal over the years, now I’ll have to settle for the Sydney Holiday inn…. 🙁

The question is, How soon will all the 40,000 point properties jump, Next year???

This devaluation makes the card virtually worthless to me and my husband. We kept it just for that perk; every year we’d combine our one free night with another night or two using our points in some really great hotel. This year, fortunately, we’ve already been issued a certificate for the Intercontinental Prague (I see there’s a dispute about whether that’s on or off the new list). So we’ll have one more chance. Last year was the Intercontinental Amsterdam and before that Hong Kong. I’ve written rapturously on search engines about these hotels so I feel IHG has gotten their money’s worth via my publicity! I’ve never found a hotel on the Points Break list to stay in. You’d really have to go out of your way to stay in some boring suburban hotel far away from anything interesting, or you’d have to hit it just right on a road trip when you don’t care that much where you stay. It puzzles me who finds those point breaks valuable. Yet, because of the free night (and Accelerate), I do go out of my way to book IHG hotels on my IHG card. Maybe it’s time to finally look into SPG and Marriott or whatever. Very disappointing, IHG!

noted! jealous of that trip…

Are existing IHG Select cardholders being demoted to the new IHG Traveler (or even the IHG Premier)? Does anyone know?