MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more.

Note: Some of the offers mentioned below may have changed or are no longer be available. You can view current offers here. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the MileValue team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

With a wallet full of credit cards, it’s best practice to commonly assess your credit card portfolio to ensure that the benefits you receive from the cards outweigh the annual fees that you pay. If not, it’s time to close that card or cards in most cases. This is normal maintenance for those of us in the points and miles world.

But in doing that maintenance, many of us have at least one, but often a few cards, that we’ll likely never close – they offer us too many benefits in return for an annual fee.

Let’s take a look at what some of those cards are for the MileValue team.

Anna Zaks

This is easy – I know exactly which three cards I’ll keep forever! Two of these are no annual fee cards and one has a high annual fee.

The Blue Business® Plus Credit Card from American Express should be in every small business owner’s wallet. The card has no annual fee (see rates and fees) and earns 2X on all purchases up to $50,000 a year, and 1X on purchases above that. If there’s a purchase that doesn’t fall into any bonus category, this is the card I use. It never leaves my wallet and allows me to earn Membership Rewards quickly.

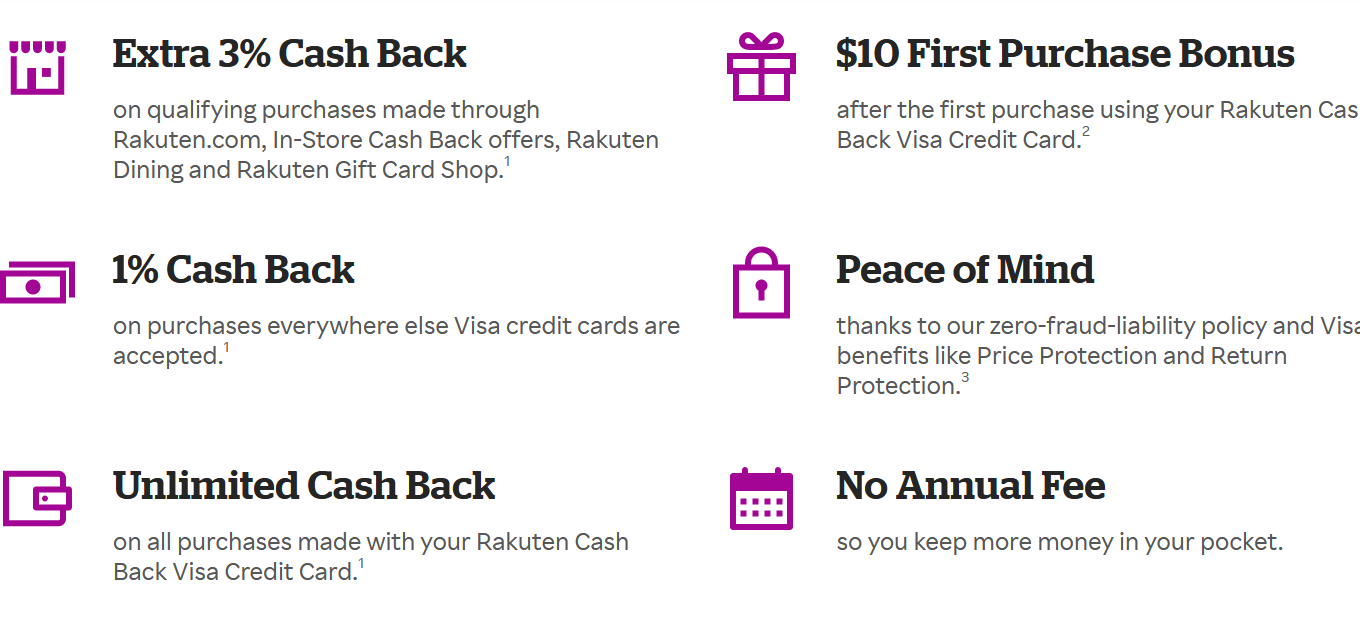

I am a huge fan of shopping portals, so every time I am buying anything online through Rakuten shopping portal I use my Rakuten Cash Back Visa Credit Card. The card has no annual fee and I only use it when I shop through the Rakuten portal. In fact it never leaves my desk, as I only use it for online purchases. I mostly shop online nowadays anyway, so that works out perfectly.

I set my Rakuten account to earn Membership Rewards points instead of cashback, so every time I click through Rakuten and use this card, I earn whatever the regular Rakuten rate is for a particular retailer, plus three additional Membership Rewards points per dollar spent.

That’s an easy way to accumulate a good stash of Membership Rewards points on the purchases you were going to make anyway without much effort.

And lastly there’s the Chase Sapphire Reserve® card. The card has a $550 annual fee and a lot of people close or downgrade it after the first year. For me, this card’s a keeper. The $300 annual travel credit helps offset the annual fee and I find other benefits such as the Priority Pass membership and the excellent travel interruption insurance super valuable. For example, my home airport has a Priority Pass-affiliated restaurant, so my husband and I love to grab a bite there before our flight.

I also use the Chase Travel portal a lot to book non-chain hotels, so that 1.5 cent-per-point redemption is invaluable. I am not big on chain hotel loyalty, and we often travel to places where there are no chain hotels at all, like small towns in Italy, so this is how I use a lot of my Ultimate Rewards points.

Anya Kartashova

My list of cards I’ll never close is pretty similar to Anna’s.

Holding The Blue Business® Plus Credit Card from American Express has been a game changer for me. Being able to accumulate 2X Membership Rewards points in all non-bonus categories and not having to pay a fee for the privilege is about as good as it gets.

The card does have a couple of downsides, such as charging foreign transaction fees, limiting double rewards to the first $50,000 per calendar year and limited acceptance rate, but these cons don’t outweigh the pros.

The second card I’ll never close might surprise you. After my credit union-issued credit card that I opened when I was 18, which I for sure will never close, my second oldest card is the Delta SkyMiles® Blue American Express Card. The card is a result of a downgrade from the Delta SkyMiles® Gold American Express Card.

Keeping my second oldest account open extends the average age of my accounts and helps my credit score stay high. This is why I’m planning on keeping this no-fee card forever. I just have to remember to make at least one purchase with it once per year.

The third card I was planning on keeping long-term was going to be The Platinum Card® from American Express. I enjoy visiting Centurion Lounges, Delta Sky Clubs and Priority Pass lounges on my trips. However, without access to Priority Pass restaurants and the rumors of not being able to bring guests to Centurion Lounges, the card has moved into a “maybe” pile, especially with a potential annual fee increase later this year.

So, my choice has changed to the Chase Sapphire Reserve®. I recently upgraded my Chase Sapphire Preferred® Card to the premium Sapphire product, and it’s likely going to stay in my wallet for a while. The flexible travel credit is easy to use, and Priority Pass lounge access and the various travel protections, such as trip delay and auto collision damage waiver on rental cars, make this card a perfect travel companion.

Travis Cormier

Choosing the three cards I’ll never close is harder than I thought. I’m going to lay out some ground rules for myself before diving into the cards. The first rule is that the benefits of the cards won’t change. Second, other cards that are better won’t hit the market. Finally, the annual fee doesn’t change.

I know that these aren’t necessarily going to hold true, but I want you to understand the mindset I’m using to approach my answer.

Without further ado, the first card that I’ll never close is the Chase Freedom Unlimited®. If anything, this card has gotten better over the past year. It has no annual fee, earns 5% cash back on travel booked through Chase Travel℠, and 3% cash back on dining at restaurants (including takeout and eligible delivery services) and 1.5% cash back on all other purchases.

In my book, this is one of the most underrated cards out there. For starters, if you’re in the know, you know that the cash back earned on the Chase Freedom Unlimited® is credit as Ultimate Rewards. If you have an Ultimate Rewards card with an annual fee like the Chase Sapphire Preferred® Card or the Chase Sapphire Reserve®, you can transfer the Ultimate Rewards from the Chase Freedom Unlimited® to the other cards and access transfer partners.

This means you can earn more points on travel than you can with any other Chase card, so long as you book through Chase Travel℠. The earning rate on dining matches that of the $550 annual fee Chase Sapphire Reserve®. And for the remaining spend you’ll earn 1.5% cash back rather than just 1X point on other cards.

Add in the fact that this is the first credit card I opened that has almost 10 years of credit history, and it makes it a no brainer that the Chase Freedom Unlimited® is a card that I’ll never close.

The next card that I’ll never close is the American Express® Gold Card. This is my go-to card for grocery spend. My family spends around $800 a month on groceries at U.S. supermarkets. The American Express Gold Card earns 4X Membership Rewards points on the first $25,000 a year of eligible purchases at U.S. supermarkets and 1X after that. With my monthly grocery budget, that adds up to about 40,000 Membership Points a year just for my grocery bill.

That’s basically a whole extra bonus every year for my typical grocery expenses. Even if I don’t use it for all of my grocery purchases, since I’ll sometimes use a card that I’m working on a new card bonus for, it is my default go-to card for groceries.

The final card that I’ll never close is The Platinum Card® from American Express. If you asked me a year or two ago, I likely would have said the Chase Sapphire Reserve®, but the CSR just isn’t keeping up with other premium cards on the market. Despite the high annual fee, the Amex Plat actually delivers on the benefits.

My home airport has a Centurion Lounge, and even with the rumors of changes in the next few years, I don’t think that impacts my decision to keep it. The perks and benefits are easy to use year after year, and I feel like I’m always getting more value than what I pay in the annual fee. With the addition of benefits while other cards have been nerfing benefits over the past year or two, I find the Amex Platinum to be a no-brainer as a card to keep year after year.

Final Thoughts

Did some of the above answers surprise you? For many new folks in this hobby, it may be surprising to see multiple responses indicating keeping cards with $500+ annual fees indefinitely. But when the benefits outweigh the annual fees, they can be a no-brainer.

Do you regularly assess your credit card portfolio? If so, let us know in the comments below what cards you’re cutting or what cards you may be looking to add!

I feel the same way about the Rakuten Visa card. It still strikes me odd that a Visa card that earns Membership Reward points.